Last Updated on: April 10th, 2025

Reviewed by Kyle Wilson

If you have a pre-existing medical condition and are considering life insurance, you might wonder if it’s even possible to get coverage. While having a pre-existing condition can complicate the application process, it doesn’t necessarily mean you can’t qualify for life insurance. In fact, there are options available, but they come with specific conditions, such as higher premiums or limited coverage. This blog will explore how pre-existing conditions impact life insurance eligibility, the types of policies available, and the steps you can take to secure coverage that fits your needs.

Get Free Quotes

Customized Options Await

Life insurance is an essential part of planning for the future, but if you have a pre-existing condition, you may be concerned about your ability to qualify for coverage. A pre-existing condition refers to any health issue or medical condition that you have been diagnosed with before applying for life insurance.

Pre-existing conditions can include chronic illnesses like diabetes, asthma, heart disease, cancer, or even mental health conditions such as depression or anxiety. Insurance companies view these conditions as higher risks, which is why they can impact your ability to qualify for a standard policy. It’s important to know what constitutes a pre-existing condition and how it may affect your eligibility or premiums. In some cases, life insurance providers may require you to provide detailed medical records or undergo additional health assessments to determine coverage terms.

Life insurance providers assess the risk of insuring applicants by considering their health status, including any pre-existing conditions. People with pre-existing conditions are seen as more likely to file a claim due to health complications, which is why insurers may charge higher premiums or impose waiting periods before coverage kicks in. Some pre-existing conditions might also make you ineligible for certain types of policies.

Understanding how insurers view these conditions can help you better navigate your options, such as applying for guaranteed issue policies or considering higher-risk policies with specific terms designed for people with health challenges.

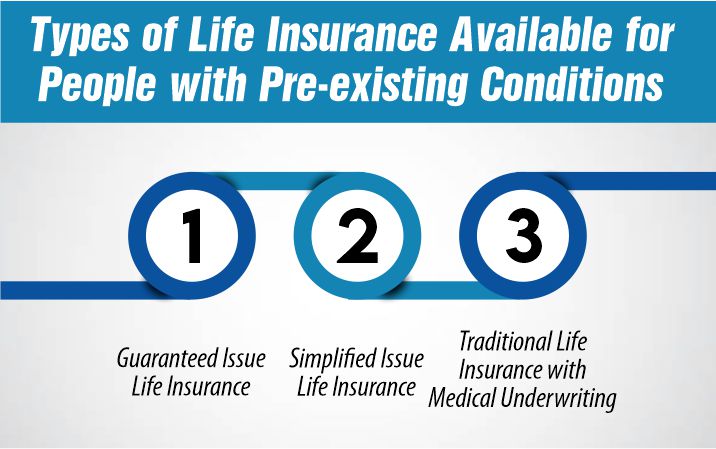

If you have a pre-existing condition, finding the right life insurance policy can be challenging, but there are options available to suit your needs. Insurance companies understand that people with pre-existing conditions still need coverage, and they offer specific types of policies to accommodate these situations. The key is understanding the types of life insurance that can provide the coverage you need while addressing any health concerns.

Guaranteed issue life insurance is one of the best options for people with pre-existing conditions who may not qualify for other policies. As the name suggests, this type of life insurance guarantees coverage, regardless of your health history. With no medical exams required, anyone can apply, and approval is typically granted as long as you meet the age requirements. However, this type of policy often comes with higher premiums and a limited payout in the first few years, making it ideal for those who need quick and guaranteed coverage.

Simplified issue life insurance is another option for individuals with pre-existing conditions. While it doesn’t require a medical exam, it does involve a short health questionnaire, where you’ll answer questions about your medical history and current health. This type of policy may be a good choice for people who have minor health issues and want coverage without the hassle of a full medical underwriting process. Though simplified issue life insurance generally offers quicker approval, it may come with higher premiums compared to traditional policies.

Traditional life insurance with medical underwriting is the most common form of coverage, but it can be more challenging to obtain if you have a pre-existing condition. This type of life insurance requires a full medical exam, including a review of your health history, which means that your pre-existing conditions will be taken into account during the underwriting process.

Depending on the severity of your condition, you may face higher premiums, or in some cases, you might be denied coverage. However, if you’re in relatively good health despite your condition, this type of policy may provide the most comprehensive coverage at competitive rates.

When applying for life insurance, pre-existing conditions can significantly impact both your approval chances and the cost of your premiums. Insurance companies assess the risks involved in insuring individuals with specific health conditions, which may affect their decision-making process. Understanding how these conditions influence the life insurance application can help you prepare for the process and make informed decisions about the best coverage options.

Having a pre-existing condition can affect your chances of getting approved for life insurance. Depending on the severity of your health condition, an insurance company might see you as a higher risk. Some individuals may face denial of coverage, while others may be offered limited or specialized policies. However, many insurance providers offer options like guaranteed issue life insurance that guarantees acceptance, despite your medical history. It’s important to research and compare different insurers to find the best policy that fits your needs.

Health conditions can have a major impact on the cost of life insurance premiums. If you have a pre-existing condition, insurance companies may charge you higher premiums to account for the potential risks. The more serious your condition, the higher your premiums might be. For example, someone with diabetes or heart disease may face significantly higher premiums compared to someone in perfect health. However, if your condition is well-managed and stable, some insurers may offer more favorable rates.

Several common pre-existing conditions can affect your life insurance application. These include chronic illnesses such as diabetes, heart disease, cancer, high blood pressure, and respiratory conditions like asthma. Insurance providers will carefully assess how these conditions impact your overall health and risk profile. Some conditions may only cause minor increases in premiums, while others might require more thorough medical underwriting or may even lead to exclusions or higher rates.

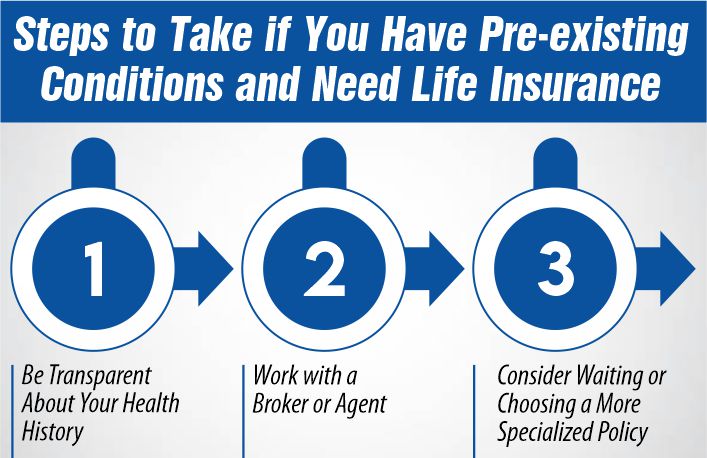

Securing life insurance with a pre-existing condition may seem challenging, but taking the right steps can make the process easier and increase your chances of getting approved. Being prepared and understanding your options will allow you to navigate the process more smoothly and find the best policy for your needs. Here are some key steps to follow when applying for life insurance with pre-existing conditions.

One of the most important steps when applying for life insurance with pre-existing conditions is being transparent about your health history. Insurance providers rely on accurate information to determine the level of risk associated with insuring you. Failing to disclose pre-existing conditions could lead to denial of coverage or even the cancellation of your policy later on.

By being honest about your health, you increase your chances of getting the coverage you need, and you avoid potential issues down the line. Always be prepared to provide medical records or documentation if requested.

Working with an experienced insurance broker or agent can be extremely beneficial when you have a pre-existing condition. Brokers can help you navigate the complexities of the insurance market and find companies that specialize in covering individuals with health conditions. They can also assist in comparing policies and premiums, ensuring that you get the best deal available.

Brokers have in-depth knowledge of insurance policies and can guide you through the application process, answering any questions you may have and helping you avoid common pitfalls.

If you’re finding it difficult to secure life insurance due to a pre-existing condition, consider waiting until your health improves or choosing a more specialized policy. Some insurers may offer better rates or coverage options after a period of improved health, so waiting could increase your chances of getting more favorable terms.

Alternatively, there are policies specifically designed for people with health issues, such as guaranteed issue life insurance or simplified issue life insurance. These policies may have higher premiums or limited coverage, but they could be your best option for getting life insurance despite pre-existing conditions.

Securing life insurance with a pre-existing condition offers several key benefits that can provide both financial and emotional peace of mind. While the process may be more challenging, the advantages are well worth considering, especially when planning for the future.

One of the primary benefits of getting life insurance with a pre-existing condition is ensuring that your family is financially secure in the event of your passing. Even if you have a health condition, life insurance provides your loved ones with the financial support they may need to cover expenses such as mortgage payments, childcare, and other essential living costs. It’s an essential tool in protecting your family’s future, especially when facing health challenges.

Having life insurance in place, even with a pre-existing condition, can provide significant peace of mind. It ensures that, in the event of an unexpected passing, your family will be taken care of without the added stress of financial burden. Knowing that you have coverage, even if it’s tailored to your specific health needs, helps ease anxiety about the future and the potential impact of your health condition on your loved ones.

Life insurance with pre-existing conditions also offers protection for final expenses, such as funeral costs and any outstanding medical bills. These expenses can add up quickly, and having a life insurance policy in place ensures that your family won’t be left to cover these costs during an already difficult time. Final expense insurance or other specialized policies can help alleviate the financial strain of end-of-life costs, allowing your family to focus on their grief rather than financial worries.

While life insurance with pre-existing conditions offers significant benefits, it’s important to be aware of the challenges you may face during the application process. Being informed about these challenges helps you better prepare for what to expect and make the right decisions for your needs.

One of the most common challenges when applying for life insurance with a pre-existing condition is the higher premiums. Insurance companies may consider you a higher risk due to your health status, which can lead to increased costs for your coverage. While these premiums may be higher, you can still find policies that suit your budget, especially if you work with a broker or agent who can help you compare options and find the best rates.

Another challenge to consider is that there may be fewer policy options available to you with a pre-existing condition. Many insurance providers offer limited coverage or specialized policies for individuals with health issues. Policies such as guaranteed issue life insurance or simplified issue life insurance may be your best options, but they often come with limitations in terms of coverage amounts or specific conditions. Understanding these options will help you make an informed decision about what works best for your situation.

Life insurance policies for individuals with pre-existing conditions may also come with exclusions or waiting periods. This means certain health conditions might not be covered initially, or there may be a waiting period before the full benefits of the policy take effect. These exclusions and waiting periods can affect how quickly your policy provides coverage and how much of your medical costs it will pay. It’s essential to review the fine print of any policy to ensure you understand what is covered and when the coverage becomes active.

Securing life insurance with pre-existing conditions is not only possible but also a smart financial move for those looking to protect their loved ones. While challenges such as higher premiums, limited policy options, and exclusions exist, there are still tailored solutions available that provide financial security and peace of mind. By understanding your options and working with an agent or broker, you can find a policy that fits your needs and budget, ensuring that your family is cared for, regardless of your health status.

Yes, it is possible to get life insurance with diabetes. However, your premiums may be higher depending on the severity of your condition. The insurance provider will likely ask for details about your diabetes management and overall health to determine your eligibility and premium rates.

Yes, some life insurance policies for individuals with pre-existing conditions may have waiting periods. This means there could be a time frame before the full benefits of the policy are available. For example, with guaranteed issue life insurance, there may be a waiting period of one or two years before the death benefit is fully paid out.

It is possible for life insurance to be denied due to pre-existing conditions, particularly if your health condition is deemed high-risk. However, there are policies available that cater specifically to people with health issues, such as guaranteed issue and simplified issue life insurance.

The best life insurance policies for people with health issues depend on your specific condition and needs. Guaranteed issue life insurance is a popular choice for individuals with serious health concerns, as it doesn’t require a medical exam. Simplified issue life insurance is another option, offering coverage with fewer health questions.

Senior Writer & Licensed Life Insurance Agent

Iqra is a dynamic and insightful senior writer with a passion for life insurance and financial planning. With over 8 years of hands-on experience in the insurance industry, Iqra has earned a reputation for delivering clear, actionable advice that empowers individuals to make informed decisions about their financial future. At Burial Senior Insurance, she not only excels as a licensed insurance agent but also as a trusted guide who has successfully advised over +1500 clients, helping them navigate the often complex world of life insurance and annuities. Her articles have been featured in top-tier financial publications, making her a respected voice in the industry.

Burial Senior Insurance provides information and services related to burial insurance for senior citizens, including policy options and end-of-life support services.

Copyright © Burial Senior Insurance 2025. All Right Reserved.

Get Free Life Insurance Quotes